Paying off student loans can be tough, especially as interest piles up over time. The good news is that there are steps you can take to make it easier and more affordable to pay off your loans.

Currently, the IRS allows you to write off the interest portion of student loan payments. If you’re a recent grad and meet certain criteria, you can deduct your student loan interest on your taxes.

Want to learn more about the student loan interest deduction and eligibility requirements? Find out everything you need to know to save when you file your taxes.

Table of Contents

What is the student loan interest deduction?What?s considered a qualified student loan?What?s considered a ?qualified education expense??What are the income phase-out ranges for the student loan interest deduction?History of the student loan relief What is the benefit of reporting student loan interest payments?What other tax information might apply to students?If I default on my student loan, does it affect my taxes?What forms do I need to fill out my taxes as a college student?How many 1098-E forms will I receive?Tax tips for studentsClaiming Your Student Loan Interest Deduction and More with TurboTax

What is the student loan interest deduction?

Luckily, taxpayers who make student loan payments on a qualified student loan may be able to get some relief if the loan they took out solely paid for higher education.

In many cases, the interest portion of your student loan payments paid during the tax year is tax-deductible. Your tax deduction is limited to interest up to $2,500 or the amount of interest you actually paid, whichever amount is less.

COVID emergency relief and the student loan debt relief announced on August 24, 2022, allowed suspension of federal loan payments at 0% interest through the end of August 2023, so you’ll most likely see a lower student loan deduction on your 2023 taxes, or even none at all.

You can deduct student loan interest if:

- You paid interest on a qualified student loan in the tax year,

- You’re legally obligated to pay interest on a qualified student loan,

- Your filing status isn’t married filing separately,

- You and your spouse, if filing jointly, cannot be claimed as dependents on someone else’s return, or

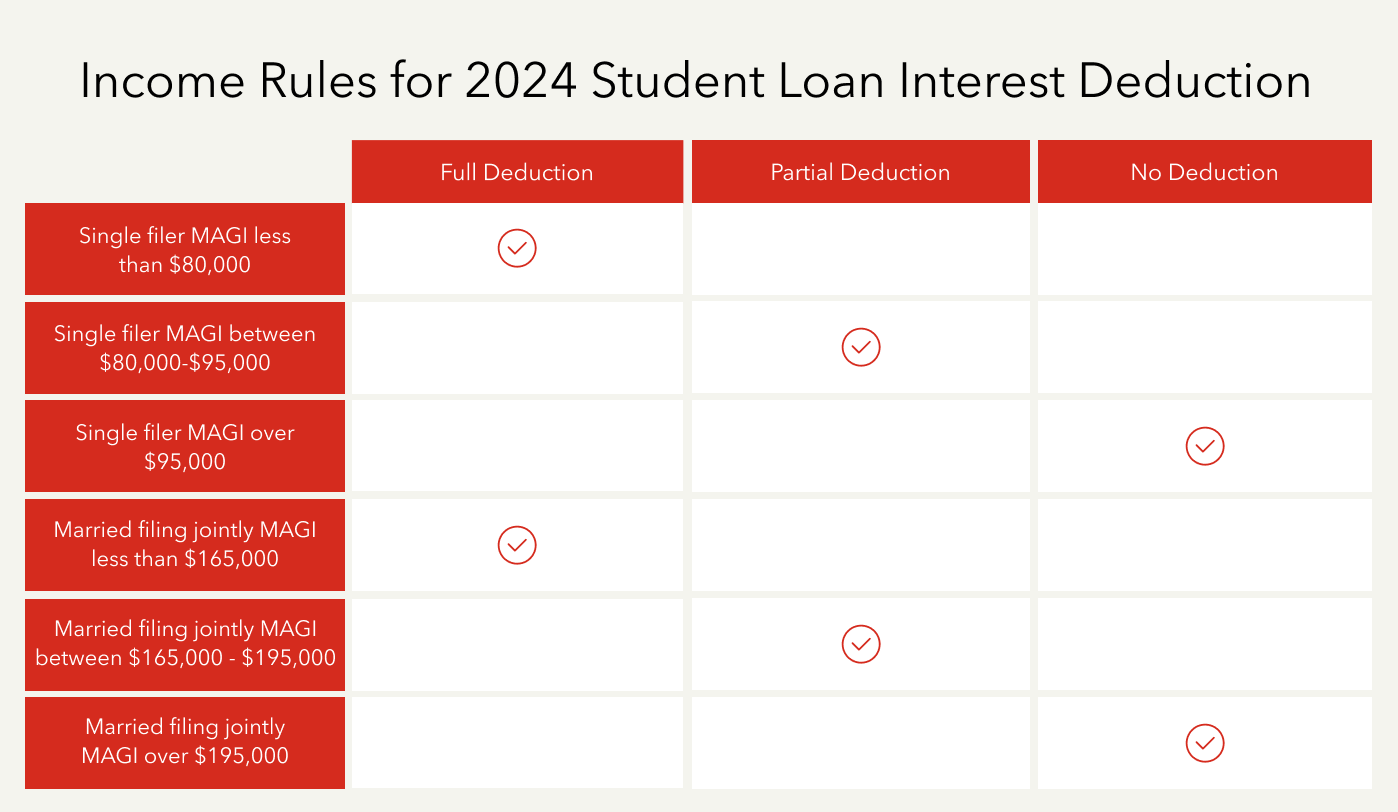

- You’re a single filer with income under $80,000 for 2024 to get the full deduction. However, your full deduction phases out (is gradually reduced) between $80,000 and $95,000 if you’re single ($165,000 and $195,000 if married filing jointly) in 2024. If your income falls above those limits, the student loan interest isn’t tax-deductible.

The other good news regarding the student loan interest deduction is that you don’t need to itemize your deductions in order to claim it. This makes sense, considering many recent college graduates aren’t itemizing tax deductions and instead claim the standard deduction.

If you paid $600 or more in interest to a single lender during the year, you should receive a 1098-E form showing how much interest you paid for that time frame. If you made student loan payments but didn’t receive a 1098-E, you’re still entitled to claim the interest deduction, but you may need to call the lender or pull up your records online.

What’s considered a qualified student loan?

In order to qualify for the student loan tax deduction, you must be making payments on a qualified loan. A qualified loan is a loan used solely for higher education. These loans must be:

- For you, your spouse, or someone who was your dependent when you took out the loan.

- Used for education during an academic period for an eligible student.

- Paid or incurred within a reasonable time period of taking out the loan.

What’s considered a “qualified education expense”?

Student loans can be used for various education-related expenses, but you have to use your student loans for the right purpose to qualify for the tax write-off. Here are some examples of qualified education expenses:

- Tuition and fees

- Room and board

- Books and other supplies required by the school

- Other expenses related to education, which can include transportation to and from school

In order to qualify for the student loan interest deduction, the money you borrowed must be used for these qualifying education expenses. Keep in mind that there are other requirements to qualify for this deduction.

What are the income phase-out ranges for the student loan interest deduction?

While the student loan tax deduction is available to most students, there are phase-out ranges depending on your modified adjusted gross income (MAGI). Let’s take a closer look at the phase-out ranges and how they affect you.

The phase-out ranges are different if you’re married filing jointly vs. separately. For 2024, the following phase-out ranges apply.

If you’re a single tax filer and your MAGI is $95,000 or more, you can’t claim the student loan interest deduction. Single filers with a MAGI between $80,000 and $95,000 can claim a reduced deduction based on their income.

Joint tax filers aren’t eligible to claim the student loan interest deduction if they have a MAGI of $195,000 or more. Joint filers who have a MAGI between $165,000 and $190,000 can claim a reduced deduction.

History of the student loan relief

Update: July 18, 2023

The Biden-Harris Administration plans to provide 804,000 borrowers with 39 Billion in automatic loan forgiveness. The Department of Education announced they will automatically discharge certain Federal student loans in income-driven repayment (IDR) plans as part of the plan announced by Biden Harris in 2022.

Borrowers who have Federal student loans in income-driven repayment (IDR) plans and have accumulated the equivalent of either 20 or 25 years of qualified payments will receive loan forgiveness for the remaining balance.

Update: June 30, 2023

The Supreme Court blocked President Biden’s plan to forgive up to $10,000 in federal student loans used to pay for college and other post-secondary education and up to $20,000 for recipients of Pell Grants.

Update: June 14, 2023

The U.S. Department of Education announced that Congress recently passed a law that would prevent further extension of the student loan payment pause. As a result, student loan interest will resume starting on September 1, 2023 and payments will be due starting October 2023.

Update: November 22, 2022

Today the Biden-Harris Administration announced another extension to the payment pause on student loan payments which could go through August 2023. The most recent extension of the pause was set to end Dec 31, 2022, but Biden’s one-time student loan forgiveness program was blocked, so the pause was extended again.

That means if blocks to Biden’s student loan debt cancellation are not resolved by June 30, 2023, student loan payments and interest will resume 60 days from June 30 through August 2023. Check back with the TurboTax blog for more up to date information regarding student loan debt.

Update: October 21, 2022

A federal appeals court has temporarily blocked Biden’s student loan forgiveness plan following an emergency motion for an administration stay which prohibits discharging any student loan debt under the cancellation plan.

While the court’s ruling is temporary, the current forgiveness timeline is frozen until the court’s briefing is due next week on the matter. If the court decides not to impose an injunction, the implementation will continue, if an injunction is imposed, loan forgiveness could be blocked while proceedings continue.

The online application for student loan forgiveness is still live and you can still apply for student loan debt relief. The administration can still collect applications during the stay. Remember when applying, only apply on the Federal Student Aid website. Check back with the TurboTax blog for more up to date information.

Update: October 15, 2022

The Department of Education has begun beta testing the student debt relief website. Borrowers are able to submit applications for the Biden-Harris Administration’s student debt relief program.

This application will allow borrowers to begin signing up before the formal website is released later this month. The link to the application is: https://studentaid.gov/debt-relief/application.

Update: August 24, 2022

President Biden, Vice President Harris, and the U.S. Department of Education announced a three part student loan debt relief plan that includes an extension of the pause on student loan payments until December 31, 2022, debt cancellation, and a proposal to create an income-driven repayment plan to help lower future monthly payments.

Find out more details about what this can mean for you here and below.

Update: April 6, 2022

The Biden Administration has extended the pause of federal student loan payments, interest, and collections through August 31, 2022.

Student loans have become a tremendous burden for many young adults and parents today. With college costs skyrocketing and little hope to cover tuition without borrowing funds in some fashion, getting stuck with those student loan payments is almost certainly a fact of life after graduation.

While you can’t typically escape student loan payments, COVID relief was available under the CARES Act, the American Rescue Plan, and executive orders to help students with federal student loans.

President Biden, Vice President Harris, and the U.S. Department of Education also announced a three part student loan debt relief plan which extended the pause on student loan payments and also provided debt cancellation, which was later blocked by the Supreme Court on June 30, 2023.

Aside from the temporary relief, are there any tax breaks that ease the burden of student loans?

Below, we’ll explore the student loan interest deduction and how you can minimize your taxes while you’re still in college.

Update: April 6, 2022

One specific provision of the CARES Act, the U.S. government stimulus and relief package designed to help Americans during the pandemic, allows employers to make student loan payments on behalf of employees of up to $5,250 per employee each year from 2021 to 2025 (totaling up to $26,250).

It’s important to know that if your employer provided you with student loan payback assistance, that money might be considered taxable income.

What is the benefit of reporting student loan interest payments?

Tax savings are the biggest benefit of reporting student loan interest payments. Since you can deduct student loan interest payments on your taxes, you can reduce your taxable income by reporting student loan interest payments.

The IRS allows you to deduct up to $2,500 in student loan interest each year, reducing your taxable income by a max of $2,500.

If you’re making student loan payments and your MAGI isn’t too high to qualify for the student loan interest deduction, you should report all student loan interest payments. This deduction, combined with other applicable write-offs, could potentially result in substantial savings.

What other tax information might apply to students?

- Your credit card interest might be deductible: If you use your credit card for qualified educational expenses, you might be able to write off the interest on your taxes. But there is one condition: every item charged to the card must be used exclusively for school-related needs, otherwise you can’t write anything off.

- Loan forgiveness can result in a tax bill: If you’re on an income-driven student loan forgiveness program, you might owe a large tax debt after the loan is forgiven. The IRS might consider the forgiven debt to be income.

- Consolidated student loans still qualify for the student loan tax deduction: If you have multiple student loans (covering multiple semesters, for example), your student loan interest is probably still deductible on your taxes.

If I default on my student loan, does it affect my taxes?

If you halt payments to your student loan servicer and your loan goes into default, there may be a few serious consequences.

For example, the government could garnish your tax refund until your debt is repaid. Other federal benefits, like any Social Security payments, would also be subject to garnishment.

What forms do I need to fill out my taxes as a college student?

Before the tax deadline, you’ll receive tax forms in the mail reporting any income you made and expenses that may be deductible. These forms might come from your previous employers, payers who you provided services to, your college, loan servicers, your bank, and any retirement accounts you have set up.

It’s a good idea to have all your documentation in front of you when you sit down to file so you report all of your income and don’t miss any tax deductions or credits you deserve. Even if you don’t receive forms reporting your income, you still have to report any income paid to you on your taxes.

Didn’t receive a form that reports your income? Don’t worry, TurboTax partners with hundreds of financial institutions, allowing you to automatically import your W-2, 1099, and 1098 information. With TurboTax W-2 import, over 150 million W-2s are supported. You can also jumpstart your taxes by snapping a photo of your W-2 and 1099-NEC, eliminating data entry.

Here are a few of the forms you might need to look out for:

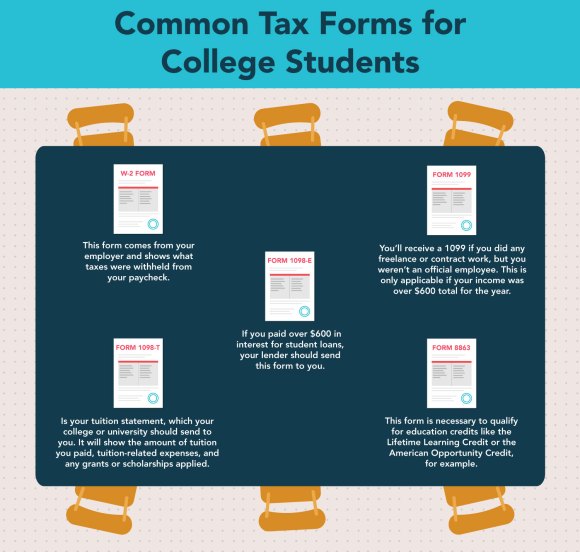

- W-2: This form comes from your employer and shows what taxes were withheld from your paycheck.

- Form 1099-NEC: You’ll receive a 1099-NEC if you did any freelance or contract work, but you weren’t an official employee. This is only applicable if your income was over $600 total for the year. Even if you don’t make $600 and don’t receive a 1099-NEC you still have to claim your income on your taxes.

- Form 1099-K: You may receive this form if you had payments processed by a third-party provider like PayPal or Venmo.

- Form 1098-E: If you paid over $600 in interest for student loans, your lender should send this form to you.

- Form 1098-T: 1098-T is your tuition statement, which your college or university should send to you. It will show the amount of tuition you paid, tuition-related expenses, and any grants or scholarships applied.

- Form 8863: This form is filed with your taxes and is necessary to claim education credits like the Lifetime Learning Credit or the American Opportunity Credit, for example. With TurboTax, you don’t need to worry about filling out forms filed with your taxes. TurboTax will fill out the appropriate forms and give you the tax deductions and credits you’re eligible for based on your entries.

Learn more about college and taxes.

How many 1098-E forms will I receive?

Generally speaking, you’ll receive a 1098-E form each time you take out a loan with a new servicer. If you took out a loan from a single servicer, you should receive a single 1098-E form that you can use to report student loan interest payments to the IRS.

Some students have student loans from multiple servicers. If that’s the case, you’ll receive a 1098-E form from each individual servicer.

Keep in mind that you can claim the student loan interest deduction whether you claim the standard deduction or itemize deductions since it’s considered an “adjustment to income” and is subtracted from your taxable income up-front before other deductions are applied.

Tax tips for students

Heading into tax season and want a few more tax tips to help you through? Read some of our tax tips below.

Tip #1: File even if you’re below the income threshold

If you make less than the IRS income filing threshold, which changes each tax year, you’re not required to file a tax return. Generally, if you made under the standard deduction for the tax year ($13,850 single or $27,700 married filing jointly in 2023 and $14,600 single or $29,200 married filing jointly in 2024 ), you aren’t required to file a tax return.

But even if you make less than the specified amount, you might still be owed a tax refund if your employer withheld taxes or if you’re eligible for some other tax credits like education credits. The IRS reports close to a billion dollars in unclaimed refunds every year, some of which belongs to college students who file their taxes.

Tip #2: Get a tax refund for work-study opportunities

Many college students end up in a work-study program to explore their career interests and get experience in their desired field. Any money you earn is considered taxable income. However, the school will withhold income taxes from your paychecks, so you may get a refund when it’s time to pay taxes.

Tip #3: Pay attention to your location

Do you attend school in a different state than your permanent residence? Then, you may have to pay taxes on any income you’ve made in another state. If you have jobs in each location, your earnings are likely subject to different tax rates. In some cases, this might work out in your favor. For example, if you work in a state without income taxes, that can help lower the overall amount of tax you pay.

Claiming Your Student Loan Interest Deduction and More with TurboTax

Don’t worry about knowing these tax rules. Meet with a TurboTax Live Full Service expert who can prepare, sign and file your taxes, so you can be 100% confident your taxes are done right. Start TurboTax Live Full Service today, in English or Spanish, and get your taxes done and off your mind.