There’s been a lot of talk – and confusion — about the homebuyer credit. Part of the confusion can be attributed to the fact that Congress made at least 3 major changes to the homebuyer credit over the last couple years. So let’s try to make some sense of it. Rather than focus on what each of the changes are, I’m going to talk about what homebuyer credits are now available and how you qualify.

But first, let’s get rid of some of the confusion brought on by the first homebuyer credit in 2008. Initially, the first-time homebuyer credit applied to homes purchased during a period in 2008. It was a $7,500 “credit” that despite its name required you to pay back the $7,500 credit over 15 years. So it wasn’t really a credit, but a loan. That is now history so you can forget about this “credit.”

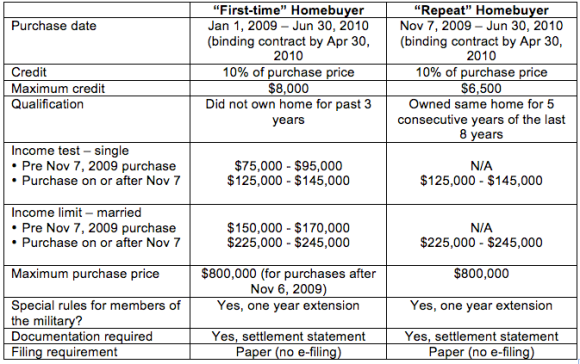

For 2009 there is now a true homebuyer credit (one that does not require you to pay it back… unless you sell it within three years) worth up to $8,000. While most of the attention has been focused on the first-time homebuyer, the credit has been expanded to include “repeat” buyers—worth up to $6,500.

To qualify for the first-time or repeat homebuyer credit, you have to meet several qualifications including home ownership and income tests. First-time homebuyers must not have owned a home in the last three years. Repeat homebuyers require home ownership for five consecutive years of the last eight years. The income test is described in the table below and is based on when you purchase your home. One thing to note about the income test is that the credit is reduced when your income exceeds the base income amount and the credit is completely wiped out when your income is $20,000 above the base amount. Not surprisingly, the homebuyer credit rules can become quite complex and that’s where TurboTax comes in. TurboTax walks you through a series of simple questions to determine eligibility and then computes your credit. You can wrack your brain trying to figure all this out, or just let TurboTax do the hard work for you. But since the Congress just passed the repeat homebuyer credit, you are going to have to wait until January to claim the credit on your return to give the IRS some time to update the tax forms. Bottom line, though, you could see your refund soar by $8,000!

This is such great news to homebuyers that it’s likely to tempt those who are looking to make a fast buck illegally. To mitigate fraud, the IRS requires documentation in the form of a completed settlement statement be attached to your tax return. As a result, homebuyers claiming the credit in 2009 will be unable to electronically file their return. While this will delay your refund by weeks, it still makes for a nice refund when it comes.

With home prices down, mortgage rates low and sweet credits available from Uncle Sam, now is a great time to purchase a home. Visit our web site for more information on the homebuyer credit.