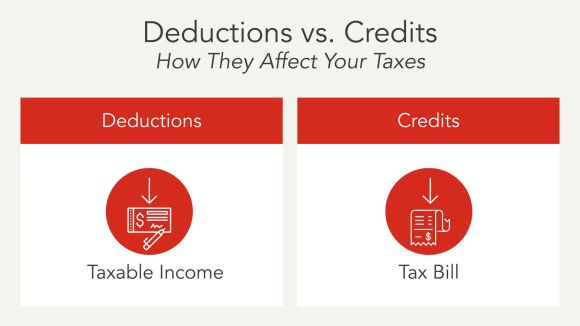

What are tax deductions? Deductions are used to reduce taxable income. And a lower taxable income reduces what you owe. Deductions are different from tax credits. Tax credits directly cut your tax bill by reducing the actual taxes owed. Both contribute to lowering your tax liability.

This guide will cover the basics of how tax deductions work. We’ll discuss how they can benefit you and how you can use them to your advantage.

We’ll tackle some of the most commonly asked questions during tax season. Then, we’ll give you a rundown on the difference between standard and itemized deductions. We’ll also highlight some of the most common deductions you’ll want to have on your radar.

With a foundational understanding of tax deductions, you’ll be better equipped to take on tax season. Use the links below or keep reading to learn more.

Table of Contents

What are tax deductions?Are tax credits the same as tax deductions?How do you know if you can claim tax deductions?8 popular tax deductionsAre the same deductions offered every year?How can you maximize your tax deductions?Lower your tax liability by leveraging deductionsWhat are tax deductions?

Tax deductions are essentially items or costs the IRS allows to reduce your taxable income on your tax return. Put simply, tax deductions lower the amount of money you must pay taxes on.A tax deduction is also referred to as a tax write-off. This is because you can “write off” or subtract these amounts from your personal taxable income.

Deductions can result in big savings. Make sure to look into which ones apply to you–we’ll cover some of the most common ones below. Keep in mind that tax laws and eligible deductions can vary from year to year. Make sure you check in on what’s on the table. That way, you can plan accordingly.

Standard vs. itemized deductions

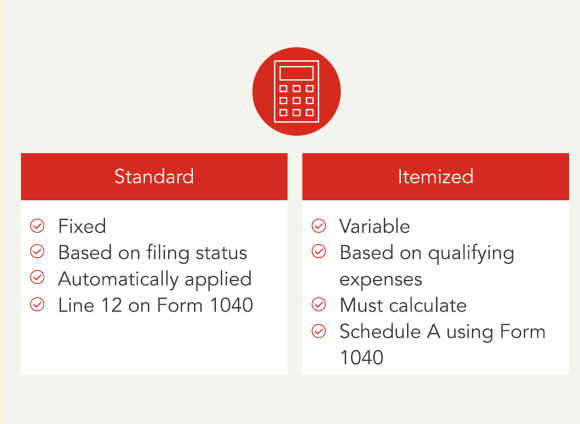

Standard and itemized deductions are two options used to reduce your adjusted gross income (AGI), which is then used to determine your taxable income. Typically, the type of deduction used will vary from year to year based upon the highest overall tax benefit provided by each deduction. Only one method can be used in any given year. The best option is to use the deduction that results in the lowest AGI. If your itemized deductions are higher, you will itemize. However, if the standard deduction is higher, you will take the standard deduction. Let’s break down the differences between each deduction.

The standard deduction is a fixed number that is based on your filing status. It can vary each tax year. It allows you to subtract a specific amount from your adjusted gross income.

The standard deduction for tax year 2024 is $14,600 for single filers (2023 is $13,850 for tax year 2023), $29,200 married filing jointly ($27,700 for tax year 2023), and $21,900 for head of household ($20,800 for tax year 2023)..

Itemized deductions are specific allowable reductions deductions that you can claim on your tax return instead of taking the standard deduction if you have total itemized deductions that are more than the standard deduction.

We’ll explore some common itemized deductions below, but a few examples include:

- Property taxes and state income taxes

- Mortgage interest

- Medical expenses

- Charitable contributions

If you itemize deductions on your tax return, you should keep detailed records and receipts. Do this for each item that you claim as an itemized deduction in case you need to substantiate the deductions you are claiming.

So, should you choose the standard or itemized deduction? Generally, TurboTax will select the method that results in the higher tax benefit for your situation. This will in turn result in a lower AGI and taxable income.

Are tax credits the same as tax deductions?

While tax credits and deductions function differently, they both help to minimize your overall taxes. Let’s dive into the differences between tax deductions vs. credits. That way, you can better understand the advantages of each.

Unlike deductions, tax credits directly reduce the amount of taxes you owe. Remember, tax deductions only reduce taxable income.

The good news is you don’t have to choose between tax deductions or credits. If eligible, you can receive both tax credits and deductions to help lower your overall tax obligation.

There are several tax credits available to you if you qualify, ranging from education to energy-saving items. A common tax credit is the Child Tax Credit, which allows parents to claim up to $2,000 per child under 17 years old. Tax credits can be either refundable or nonrefundable. The Additional Child Tax Credit is refundable up to $1,600. That means you could receive this amount as a refund even if you don’t have a tax liability.

How do you know if you can claim tax deductions?

The first thing you should do is research the common deductible expenses and ensure that you meet the criteria for each.

If your total itemized deductions exceed the standard deduction, itemizing will likely give you the best tax outcome. You’ll claim itemized tax deductions on Schedule A of your Form 1040. The Schedule A form is used to calculate and report each deduction separately to calculate your total itemized deductions.

However, if the standard deduction amount is higher than itemized deductions, TurboTax will select the standard deduction for you. The standard deduction is reported on Form 1040, line 12. Unlike itemized deductions, the standard deduction doesn’t require documentation of specific expenses.

Don’t worry about knowing whether to choose the standard deduction versus itemized deductions. TurboTax will ask you simple questions about you and give you the tax benefits that give you the best tax outcome.

8 popular tax deductions

What are common deductions you should keep an eye out for? These popular tax deductions are an easy way to reduce your taxable income. In turn, they can minimize the amount of money you owe.

Some deductions serve as incentives and include items, such as:

- Owning a home

- Donating to charity

- Medical Expenses

Deductions are as varied as taxpayers. Take a look at the list below to start planning which deductions you’re going to take advantage of:

Itemized Deductions

- Medical expense – itemized deduction

You can deduct qualifying medical expenses as part of your itemized deductions if they exceed 7.5% of your AGI. This can include costs related to medical care and includes prescriptions.

2. State Income Tax, Sales and Local Tax, and Property Taxes – itemized deduction

You can deduct state income taxes or sales and local tax and property taxes you paid. Under tax reform, you can only deduct up to $10,000 for property taxes and state and local income taxes or sales taxes paid.

3. Mortgage interest – itemized deduction

If you’re a homeowner, you can deduct the interest paid on your mortgage loans. This can help not only reduce your taxable income but also make homeownership a more affordable process.

- Charitable contributions – itemized deduction

You can also deduct donations made to 501(c)(3) nonprofit organizations throughout the year. A charitable contribution helps to reduce your taxable income depending on the value of your contribution.

Above the Line Deductions

- Student loan interest – above-the-line deduction

This deduction allows you to write off a certain amount of paid interest on qualified student loans. Deducting student loan interest can help ease the financial burden of student loan repayment. These payments are reported on Schedule 1, part II, line 21 and are used to reduce your adjusted gross income.

- IRA contributions – above-the-line deduction

Have a traditional individual retirement account (IRA)? You may be able to deduct any contributions that you made throughout the tax year. These contributions are reported on Schedule 1, part II, line 20 and are used to reduce your adjusted gross income.

- HSA contributions – above-the-line deduction

A health savings account (HSA) helps those with high health plan deductibles manage their money for medical expenses. If you contribute to a HSA, you might be able to deduct it from your taxable income on Schedule 1, part II, line 13. If the contributions are made via your employer, then the HSA contribution will be reported on your W-2 Form in Box 12.

Self-Employed Deductions

- Business expenses for self-employed individuals

A business expense can be anything from office supplies to travel costs. If you’re self-employed, you can write off necessary expenses for operating your business. These expenses are used to offset any income earned from your business and are reported on Schedule C.

Are the same deductions offered every year?

While some tax deductions may stay the same from year to year, others can change due to updates in tax regulations or the economy. For any given tax year:

- New deductions can be introduced

- Existing deductions can be modified

- Certain deductions might be removed

How can you maximize your tax deductions?

Optimizing your tax deductions requires strategic planning, organization, and knowledge of eligible expenses.

Tax deductions can include many activities. You might be better off claiming the standard deduction if you don’t have significant itemized deductions.

On the other hand, you might choose to itemize deductions to maximize your potential savings. When itemizing, you can proactively plan for additional expenses in the upcoming year.

During the years that you’re planning to itemize, explore all deduction opportunities, including those for:

- Homeownership

- Medical costs

- Charitable donations

Additionally, be aware of commonly overlooked deductions and credits that may apply to your situation. You might have the opportunity to benefit from unexpected costs like:

- Health insurance

- Investments in retirement accounts

- Student loan interest

As part of your tax strategy, you could bunch regular expenses into one tax year instead of spreading them out. Bunching your deductions also helps to maximize their value since some tax deductions require a minimum expense to qualify.

Another strategy to maximize your tax deductions includes keeping organized records of all your eligible costs. During the year, maintain copies of large and small expenses so you have them ready come tax time.

Lower your tax liability by leveraging deductions

Reduce the financial stress of tax season by leveraging the power of deductions. By lowering your taxable income, deductions unlock opportunities to save money–who wouldn’t want that?

It’s good to have a basic understanding of the rules. That said, we make it easy to figure out if you qualify for deductions when you use TurboTax. No matter what moves you made last year, TurboTax will make them count on your taxes. Whether you want to do your taxes yourself or have a TurboTax expert file for you, we’ll make sure you get every dollar you deserve and your biggest possible refund – guaranteed.